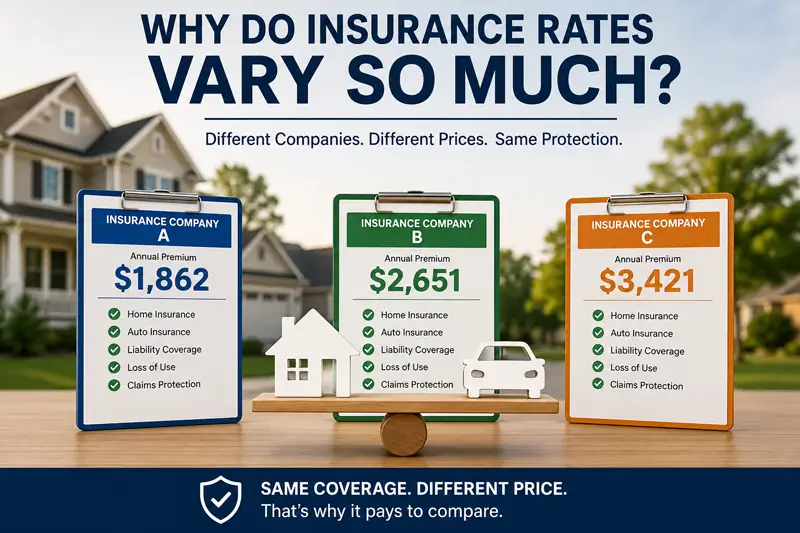

One of the questions we hear most often at our agency is: "Why is one…

Protecting Your Vacation Home

If you have the good fortune to have a vacation home, it’s critical to insure it since you won’t be in residence all year. If damage occurs, you may not even know it and if you carry a mortgage on the home, insurance will be a requirement. Since it’s a second home, you’ll need a separate policy on the structure and if you also utilize it as a short-term rental as many families are doing, additional coverage may be needed.

High Risk

Insurance companies view vacation homes as higher-risk dwellings for several reasons. They’re not occupied year-round and neighbors that might be able to report a problem may also be in residence part-time. Beachfront homes are at increased risk of vandalism and squatters are a potential problem, especially in today’s housing climate. Scams are also rampant in which unscrupulous individuals rent homes they don’t own.

Named Perils

Vacation home insurance policies are different than your primary homeowner’s policy. The insurer may create a policy for you that is based strictly on named perils. The policy will spell out what events are covered, such as fire and smoke, hail, theft, wind, lightning and explosions. You also have the option of purchasing a policy that covers all risks, including hurricanes, unless its specifically excluded.

Liability

The policy may include liability coverage in the event that someone is injured on your property. It’s coverage that’s well worth the money. There are numerous examples of intruders being injured while on a property illegally and then suing the homeowner.

Cost

The cost will depend on several factors that include location, condition and age, and property type. Vacation homes that are in areas prone to forest fires, mudslides, storm surges, and flooding from hurricanes will obviously come with expensive premiums. Older homes and those where regular maintenance has been neglected will also cost more to insure.

Beachfront homes will be more expensive to insure than a cabin in the woods, and larger homes will also be more costly to insure. Think carefully about the home’s amenities. Hot tubs, swimming pools, exercise equipment, and docks and piers, along with small watercraft and technology enabled appliances and similar items will increase the cost of insuring your vacation home.

For more information about how The Sena Group can help you with any

of your insurance needs, please contact us at 561-391-4661.

We can be found on Social Media at the following links.

The Sena Group

6501 Congress Ave., Ste. 100

Boca Raton, FL 33487

Related Posts