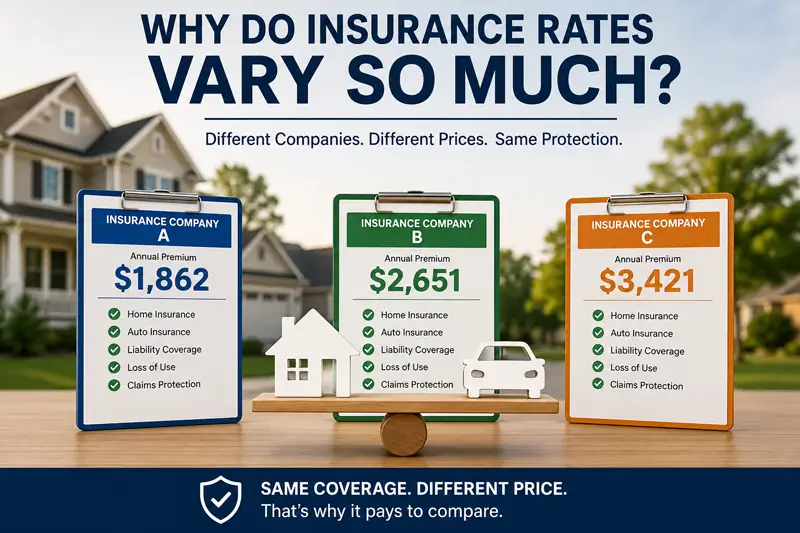

One of the questions we hear most often at our agency is: "Why is one…

Insuring Your First Home

You’ll want to provide as much protection for your home as possible, without spending a fortune, but understanding exactly what you’re purchasing in your policy can be confusing. Insurance can also be expensive, especially in South Florida where the danger of hurricanes, flooding and sinkholes are common problems.

Fire, Flood and Wind

A homeowner’s policy will be required if you’re obtaining a mortgage and there may be very specific coverage involved. It provides protection for a variety of damages that includes fire, wind, and storm damage. However, to be protected against flooding, you’ll need to purchase a separate policy, typically from the National Flood Insurance Program operated through FEMA. Many companies in Florida no longer offer any flood insurance coverage.

Shop Around

Don’t purchase coverage with the first insurance company with which you consult. Compare rates and consider obtaining home and auto coverage from the same insurer for discounts. You can purchase home insurance prior to closing on the home and some lenders even require it. Not having coverage can delay your closing.

Obtaining coverage early also gives the insurance agency time to properly value the property. That’s especially important if the house contains features such as rare woodworking, elaborate sound and entertainment systems, or technology. An early appraisal will aid in preventing you from paying too much or not having sufficient coverage.

Market vs. Replacement Value

Most policies are written to cover the current cost of repairing or replacing a home, known as market value. That cost increase significantly, even a year from now. You can insure your home and its contents for the replacement cost instead. It’s a good idea to ensure your policy includes an inflation guard so coverage rises as building costs increase.

What Isn’t Covered

It’s equally important to know the limitations of your coverage and your deductible – what your portion of the costs will be if you need to file a claim. Situations that are considered preventable with reasonable home maintenance include wear and tear on old roofing, insect infestations, and mold. Your insurance won’t cover those instances and some others.

For more information about how The Sena Group can help you with any

of your insurance needs, please contact us at 561-391-4661.

We can be found on Social Media at the following links.

The Sena Group

6501 Congress Ave., Ste. 100

Boca Raton, FL 33487

Related Posts