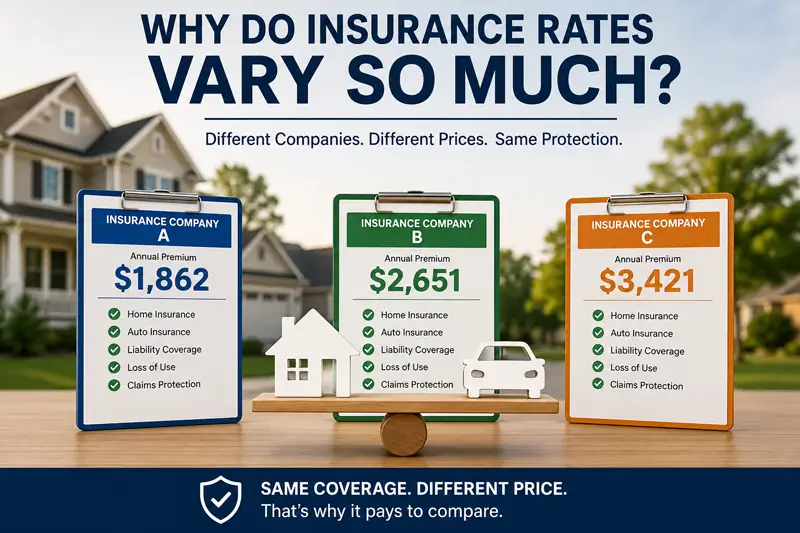

One of the questions we hear most often at our agency is: "Why is one…

Common Types of Uninsurable Risk

Insurance policies protect homes and possessions for an extensive array of disasters, but insurance companies always include exclusions. There are some types of events and circumstances that insurers think it would present too much of a financial risk for the company.

Flooding

South Florida is prone to hurricanes that create flooding due to rain and storm surges that insurers won’t cover. Those that need flood insurance can obtain it through the National Flood Insurance Program (NFIP) administered through FEMA.

Owner Acts

Damage to property that’s directly related to something a homeowner did or didn’t do is excluded. That can include lack of maintenance, failure to have a known problem remedied, or damage deliberately inflicted by the policy holder.

Shifting Soil

Shifting and settling of home foundations aren’t covered, even if they result in structural damage. The soil in Florida is subject to swelling and shrinking depending on the moisture content. If a home collapses, that’s covered.

Disasters

There are exclusions for manmade disasters that include acts of war, a nuclear hazard, and exposure to radiation. Natural disasters encompass floods, earthquakes and mudslides. Most policies won’t cover damage from sinkholes, but insurance companies are required by Florida law to cover catastrophic ground cover collapse.

Dog Breeds

Many insurance companies refuse to provide coverage – or charge extra – for homes with certain dog breeds. Dogs with a reputation for biting, damage to property, or aggressiveness can also be excluded.

Code Violations

For people that like to take a DIY approach to home repairs, if the work violates safety codes the damage won’t be covered.

Insects and Vermin

Infestations by insects, rodents and wildlife are exclusions and won’t be covered. However, insurers will typically pay for repair and remediation after the damage has already occurred.

Mold

Warm, moist conditions create the perfect environment for mold growth, both of which Florida has in abundance. Policies may or may not have an exclusion for mold, depending on the circumstances.

Home-Based Business

A homeowner’s policy may or may not provide protection for a home business operated out of the home. Coverage for injuries to people while in the office or loss of equipment will depend on how the policy is written.

For more information about how The Sena Group can help you with any

of your insurance needs, please contact us at 561-391-4661.

We can be found on Social Media at the following links.

The Sena Group

6501 Congress Ave., Ste. 100

Boca Raton, FL 33487

Related Posts