One of the questions we hear most often at our agency is: "Why is one…

The Impact of Credit Scores on Insurance Premiums

Your credit score is a powerful financial indicator that extends beyond loan approvals and interest rates. In the world of insurance, credit scores play a significant role in determining premiums. In this blog, we’ll explore the impact of credit scores on insurance rates and provide valuable tips on how to improve your credit to secure better insurance rates.

Understanding the Connection: Credit Scores and Insurance Premiums

Insurance companies use credit scores as one of the factors in assessing risk. Studies have shown a correlation between credit history and the likelihood of filing insurance claims. As a result, individuals with higher credit scores are often deemed lower-risk policyholders, leading to lower insurance premiums.

The Credit Score-Influence on Different Types of Insurance

- Auto Insurance: A good credit score can result in lower auto insurance premiums. Insurers believe that individuals with higher credit scores are more responsible and, therefore, less likely to engage in risky behavior while driving.

- Home Insurance: Homeowners with higher credit scores may enjoy lower home insurance premiums. Insurers perceive responsible financial habits as an indicator of responsible home maintenance and reduced risk of claims.

- Life Insurance: While credit scores may not directly impact life insurance premiums, a good credit history can reflect positively on your overall financial health, potentially leading to better rates.

Tips for Improving Credit Scores: A Path to Lower Premiums

- Monitor Your Credit Report: Regularly check your credit report for inaccuracies or fraudulent activities. Dispute any errors promptly to ensure an accurate representation of your creditworthiness.

- Pay Bills on Time: Timely payments have a significant impact on your credit score. Set up reminders or automatic payments to avoid late payments and potential negative effects on your credit.

- Reduce Credit Card Balances: High credit card balances relative to your credit limit can negatively impact your credit score. Aim to keep your credit utilization ratio low by paying down balances.

- Diversify Your Credit: A diverse credit mix, including credit cards, installment loans, and retail accounts, can positively influence your credit score. However, avoid opening multiple new accounts in a short period.

- Establish a Strong Financial History: The length of your credit history is a factor in your credit score. Maintain long-standing accounts, even if you use them sparingly, to demonstrate stability.

Shop Around for Insurance Rates: Find the Best Deal

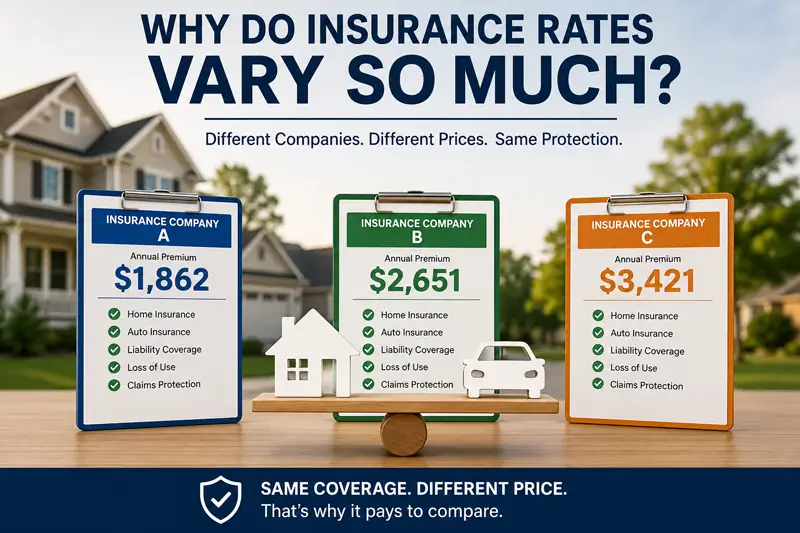

Regardless of your credit score, it’s essential to shop around for insurance rates. Different insurance providers weigh credit scores differently, and you may find significant variations in premium quotes. Obtain quotes from multiple insurers to identify the best deal for your coverage needs.

Understanding the relationship between credit scores and insurance premiums empowers you to take control of your financial well-being. By improving your credit score through responsible financial habits and shopping around for the best insurance rates, you can unlock potential savings on your premiums. Remember, a strong credit history not only benefits your insurance costs but also contributes to overall financial health.

For more information about how The Sena Group can help you with any

of your insurance needs, please contact us at 561-391-4661.

We can be found on Social Media at the following links.

The Sena Group

6501 Congress Ave., Ste. 100

Boca Raton, FL 33487

Related Posts