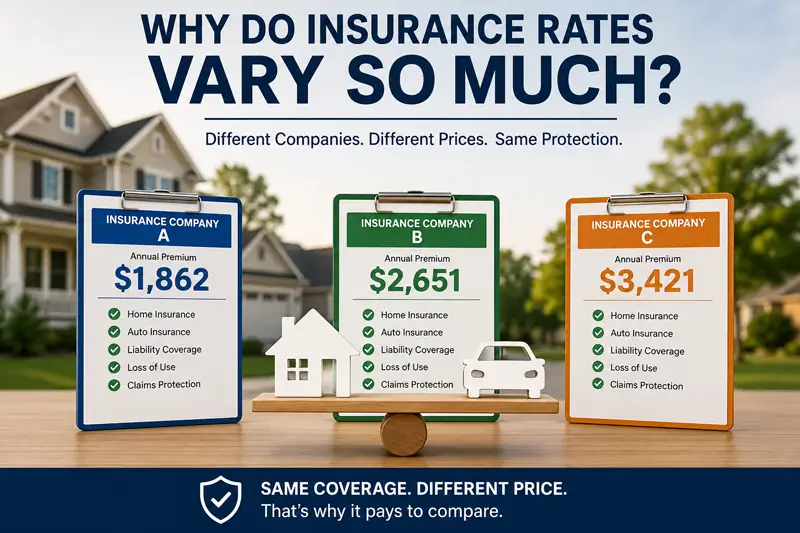

One of the questions we hear most often at our agency is: "Why is one…

Home Insurance 101

Owning a home is a significant investment, and protecting it against unforeseen events is crucial for financial security. Home insurance serves as a safety net, providing coverage for a range of risks that homeowners may face. In this comprehensive guide, we’ll delve into the basics of home insurance, explore coverage types, and offer valuable insights on how to safeguard your home against unexpected events.

Understanding Home Insurance: The Basics

Home insurance, also known as homeowner’s insurance, is a financial protection policy that covers your home and its contents against various perils. These perils may include fire, theft, vandalism, natural disasters, and liability for accidents that occur on your property. Home insurance typically consists of multiple coverage components designed to provide comprehensive protection.

Coverage Types: Breaking Down the Components

- Dwelling Coverage: Protects the structure of your home, including the foundation, walls, roof, and built-in appliances. This coverage ensures that your home can be repaired or rebuilt in the event of covered damage.

- Personal Property Coverage: Covers your belongings, such as furniture, electronics, clothing, and other personal items, against damage or theft. It’s important to create an inventory of your possessions to facilitate the claims process.

- Liability Coverage: Offers financial protection in case someone is injured on your property, and you are found responsible. This coverage includes legal expenses and medical bills for the injured party.

- Additional Living Expenses (ALE) Coverage: Provides assistance with temporary living expenses if your home becomes uninhabitable due to covered damage. This can include hotel bills, meals, and other necessary costs.

Factors Affecting Home Insurance Premiums: Understanding Costs

Several factors influence the cost of home insurance premiums, including the location of your home, its age, construction materials, and your credit score. Additionally, the coverage limits you choose, deductible amount, and any optional endorsements or riders can impact the overall cost.

Mitigating Risks: Protecting Your Home

- Home Security Measures: Installing security systems, smoke detectors, and deadbolt locks can reduce the risk of theft and fire, potentially lowering insurance premiums.

- Regular Maintenance: Keeping your home well-maintained, including repairing roof damage, fixing leaks, and addressing structural issues, can help prevent damage and demonstrate responsibility to insurers.

- Disaster Preparedness: Know the risks in your area and take steps to mitigate them. For example, if you live in an area prone to flooding, consider purchasing flood insurance as it’s not typically covered under standard home insurance.

- Review and Update Coverage: Regularly review your home insurance policy to ensure it reflects any changes in your home’s value, improvements, or changes in personal circumstances.

Home insurance is a fundamental aspect of responsible homeownership, offering protection against the unexpected. By understanding the basics of home insurance, the various coverage types, and implementing proactive measures to safeguard your home, you can ensure that your investment is well-protected. Take the time to review and update your policy regularly, adapting it to changes in your life and maintaining peace of mind in the face of life’s uncertainties.

For more information about how The Sena Group can help you with any

of your insurance needs, please contact us at 561-391-4661.

We can be found on Social Media at the following links.

The Sena Group

6501 Congress Ave., Ste. 100

Boca Raton, FL 33487

Related Posts