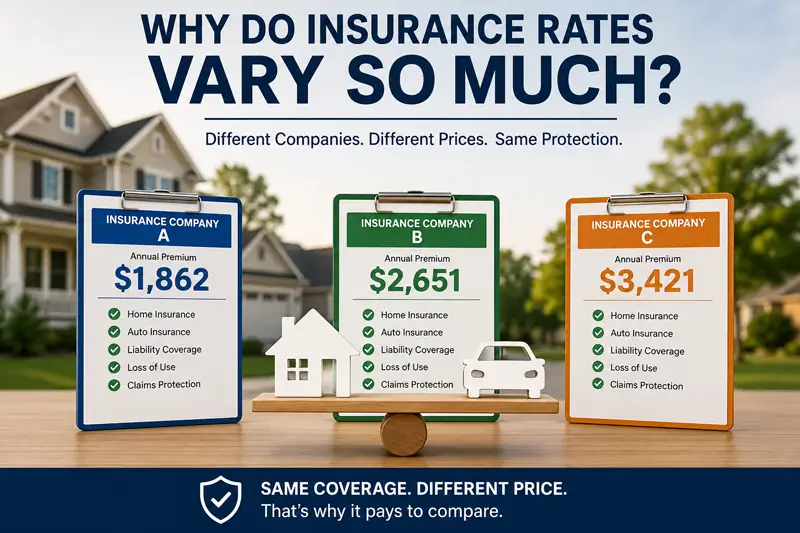

One of the questions we hear most often at our agency is: "Why is one…

Homeowners Insurance Deductibles Explained!

A homeowner’s insurance policy is essential and an expense that many new home owners don’t consider when searching for their dream house. It’s important that homeowners understand what a deductible is, how it works, and their choices when choosing the amount.

What is a Deductible?

The deductible on a homeowner’s policy is the amount that individuals will be required to pay out-of-pocket if a claim is filed for damages. This is the amount that homeowners pay before the insurance company covers the remainder of the costs. There are deductible amounts for damages to the home, as well as the contents.

Types of Deductibles

There are typically two types of deductibles that homeowners encounter. One is a standard deductible that usually ranges from $500 to $2,000 for most types of losses. There are also percentage deductibles that run from 1 to 5 percent of the total costs associated with the damage. Percentage deductibles are more likely to be associated with damage related to wind, hail, flooding, tornadoes, and hurricanes.

How They Work

A deductible is typically paid on a per-claim basis. Homeowners would have to pay the applicable deductible each time they make a separate claim. In Florida, homeowners may have a hurricane deductible that’s applicable per season rather than per claim. When hurricane deductibles are met on a first claim in a given year, an all-peril clause – or other standard deductible amounts – may apply for any other hurricane damage within the same year. Other types of damage from weather conditions may have similar clauses.

Coverage

Homeowner’s insurance also covers personal liability in the event that someone is injured while in the home or on the property whether it’s a postal worker or someone that strays onto the property. The homeowner is not required to pay a deductible in those instances.

Setting Deductibles

Homeowners are often tempted to choose a higher deductible to lower their overall insurance costs. It can be a costly mistake. Homeowners should choose a deductible amount that they can comfortably afford should they need to make a claim.

For more information about how The Sena Group can help you with any

of your insurance needs, please contact us at 561-391-4661.

We can be found on Social Media at the following links.

The Sena Group

6501 Congress Ave., Ste. 100

Boca Raton, FL 33487

Related Posts